New $20M Capacity addresses severe convective storm and named wind storm risk as clean energy projects continue to scale

SAN FRANCISCO – August 28, 2025 – kWh Analytics, the market leader in Climate Insurance, today announced the expansion of its insurance solutions with new Excess Natural Catastrophe coverage through its licensed insurance entity, Solar Energy Insurance Services, Inc., specifically addressing the growing need for severe convective storm protection in the renewable energy market.

This new offering complements kWh Analytics’ existing property capacity, which provides 100% operational and construction coverage for solar, wind, and battery energy storage assets. The Excess Natural Catastrophe layer will provide up to $20M in additional capacity specifically covering damage from severe convective storms and named windstorms in non-coastal regions.

“Our loss database reveals that hail accounts for 73% of total solar industry losses by damage amount,” said Jason Kaminsky, CEO of kWh Analytics. “As renewable projects grow in size and tax-equity investors and lenders require higher insurance limits, we’re addressing a critical market gap with this specialized excess layer solution.”

A cornerstone of kWh Analytics’ approach is rewarding resilience through its underwriting process. Projects that implement protective measures such as hail stow capabilities, reinforced module characteristics including glass thickness, and proper O&M protocols will benefit in the excess layer, just as they do in primary coverage.

“Resilience should be rewarded at every level of coverage,” said Isaac McLean, Chief Underwriting Officer at kWh Analytics. “Our Excess Natural Catastrophe offering evaluates the same resilience factors we consider in primary coverage, and we request asset owners and sponsors provide us details of their hardening strategies so we can appropriately credit their risk mitigation efforts.”

To provide a standardized framework for evaluating hail resilience and offer insurance credit for protective measures, kWh Analytics and VDE Americas have developed the Hail Stow and Risk Evaluation tool. This assessment examines critical factors, including panel specifications, tracker stow angles, forecasting systems, and testing protocols. Projects demonstrating robust hail defense strategies through this evaluation can secure more favorable terms, even in the excess layer.

Solar Energy Insurance Services, Inc., a kWh Analytics company, a leading Climate Insurance provider, underwrites property insurance and revenue firming products for renewable energy assets. Our proprietary database of 300,000+ zero-carbon projects and $100B in loss data fuels advanced modeling and insights, enabling precise underwriting decisions. This data-driven approach incorporates resiliency measures in risk evaluation, promoting sustainable practices in the renewable energy sector.

Trusted by 11 global (re)insurance carriers, we’ve insured over $50 billion in assets to date. Our tailored solutions further our mission of providing best-in-class Insurance for our Climate. Recognized by InsuranceERM Climate and Sustainability Awards, kWh Analytics continues to pioneer in the renewable energy insurance sector.

The renewable energy industry is always thinking in the long term. We build projects designed to operate for 30+ years, knowing they’ll face whatever weather patterns, administrations, and market conditions emerge over those decades.

Right now, that long-term thinking feels more critical than ever. Recent policy shifts and climate reports have created uncertainty, but they’ve also reinforced something we’ve always known: this industry succeeds when we build resilient infrastructure that can weather any storm—literal or figurative.

The reality is that our projects are getting larger while extreme weather is getting more severe. A single hail event can now represent tens of millions in losses on utility-scale installations, and utilizing insurance as a risk transfer mechanism is now more critical than ever. When traditional insurance markets began to pull back from renewables, leaving coverage gaps that threatened project financing, we had a choice to either accept that constraint or find a way around it.

That’s why we’re launching Excess Natural Catastrophe coverage: up to $20 million in additional capacity, specifically designed to cover losses resulting from hail, severe convective storms, and named windstorms for solar, wind, and BESS assets. This is in addition to our excess capacity for wildfire, earthquake, and flood, which we already write. Excess layers are designed to protect a project in case it receives damages that exceed the limits of the primary layer. It’s not always going to be necessary for every site, but when hail alone accounts for an estimated 73% of total losses in the solar industry, it can provide an extra sense of security, especially in high-hazard hail and hurricane zones.

We’re applying the same philosophy we’ve always used: resilience should be rewarded. Projects that invest in hail stow systems, quality equipment, and robust O&M protocols get better terms. We’ve developed our Hail Stow and Risk Evaluation form in partnership with VDE Americas to standardize how we assess these protective measures, creating a clear framework for recognizing and rewarding the investments that asset owners make in protecting their projects.

Launching this product is a significant milestone for kWh Analytics, and I’m grateful for our team, our carriers, and reinsurance partners who helped make this happen. Insurance should be a catalyst, not a constraint, for the growth of clean energy, and we’re proud to play a role in enabling that progress. The challenges facing renewable energy are real, but so is our commitment to building risk transfer solutions that outlasts them.

Originally published by PVMag

By Garvin Jones, kWh Analytics, and Amanda Lania, CAC Specialty

As the renewable energy sector matures, asset owners are increasingly investing in advanced technologies that protect their solar, wind, and battery assets. Investments are being made into thicker glass photovoltaic modules to prevent hail damage, advanced hail stow systems that better weather hail and wind events, and sophisticated vegetation management protocols that prevent brushfire. Yet, many find themselves asking a familiar question: “We’re doing all the right things from a technology standpoint, but where’s the insurance credit for our efforts?”

Technology is only one part of the resilience equation; how a renewable energy site actually operates and maintains its assets is just as important as the equipment itself. While the industry has focused heavily on equipment specifications and design standards, it is the human element that determines whether resilient technologies actually deliver their intended protections.

Consider hail mitigation as an example. An asset owner might invest in 3.2mm tempered glass modules and state-of-the-art tracking systems capable of 75-degree hail stow. From a technology perspective, this represents best-in-class resilience. But, does the site effectively execute proper stow protocols when severe weather threatens? Are operators monitoring weather alerts 24/7, or do they have automated programs or third-party experts that do so? Do they have redundant notification systems or overrides in place? More importantly, can they prove it?

The missing piece is often demonstrating that the technology is being used correctly and consistently. This behavior-versus-technology disconnect affects virtually every aspect of renewable energy risk management – from vegetation management to battery system monitoring to equipment maintenance protocols.

The renewable energy insurance market is beginning to adopt a premium differentiation model, where underwriters give credit to best-in-class assets that can prove their resilience towards damaging hail, hurricane, wind, and fire risks. However, these same underwriters want to see evidence of proactive damage prevention rather than reactivity. This means moving beyond equipment specifications to document actual operational performance.

Comprehensive documentation is perhaps the most critical element in demonstrating resilient behavior to brokers and insurers. Historically, the solar industry has not issued standardized guidelines on documenting and sharing ongoing operational practices like hail stow logs. Often times these practices aren’t visible to underwriters. For asset owners, it is important to keep several key considerations in mind:

Hail Stow Execution: Stow refers to tilting solar modules to a high degree angle to reduce the risk of hail or wind damage. Having hail stow capability is only the beginning. Ensure that historical stow logs show successful execution during weather events, documentation of testing protocols, and evidence of redundant alert systems. Some forward-thinking asset owners are now providing reports showing every weather event logged where stow was triggered, creating a track record of operational reliability.

Vegetation Management: While many sites have vegetation management plans, the quality and execution vary dramatically. Best-in-class operators maintain detailed logs of vegetation control activities, implement proactive monitoring around critical equipment like inverters and transformers, and coordinate closely with local fire departments. The difference between a routine mowing schedule and a comprehensive fire prevention program can be substantial from an insurance perspective.

Equipment Maintenance: Robust operations and maintenance (O&M) protocols go beyond scheduled maintenance to include predictive monitoring, rapid response capabilities, and comprehensive spare parts programs. Asset owners who can demonstrate systematic equipment monitoring with documented response times and resolution rates present a reduced risk profile versus those demonstrating basic maintenance controls.

Emergency Response: Whether dealing with severe weather, equipment failures, or fire risks, having documented emergency response protocols with evidence of staff training and coordination with local response authorities demonstrates operational excellence.

Effective documentation for the above may include:

Operational logs showing equipment performance, maintenance activities, and response times

Weather event records documenting stow execution and system performance during severe conditions

Training records for operations staff and emergency response protocols

Vendor management showing quality control measures for contractors and service providers

Performance metrics tracking availability, response times, and operational KPIs

The challenge for many asset owners is guaranteeing insurers can see and understand the operational excellence beyond just equipment specifications. This is where systematic data collection and reporting becomes essential for translating operational excellence into insurance value.

Insurance Value

For asset owners wondering whether operational excellence translates into tangible insurance benefits, the answer is increasingly yes, when properly documented and communicated. Insurance markets are beginning to develop more sophisticated approaches to pricing resilience that account for both technology and behavior.

For one insured, the benefit of providing a well-documented stow procedure resulted in a 40% reduction in their account’s quoted Natural Catastrophe rate. The procedure included automation with 24/7 human monitoring and multiple stow contingency plans. The supporting documentation outlined each project’s specific stow procedures, the technology and weather monitoring tools being utilized, as well as the protocol to follow in the event the primary stow plan failed.

Another insured received a 25% discount in attritional rating across their portfolio as a direct result of their well-demonstrated O&M practices and superior asset management. The best-in-class asset management was supported by a favorable loss history for an account with over 200 locations and a variety of O&M contractors.

The tangible benefits for well-documented operational excellence go beyond just premium rate reductions. For example, a well-documented flood mitigation plan and site design can be the difference between insurance markets extending flood coverage for a given location or potentially excluding coverage altogether. In other instances, the benefits can be seen through larger line size capacity offerings, lower deductibles, or increased natural catastrophe sublimits to help insureds meet their lender required coverages.

The path forward involves three key elements.

Investing in appropriate hardening technology

Developing robust operational protocols to utilize that technology effectively

Implementing documentation systems that, when shared, allow insurers to assess and price operational risks properly

As the renewable energy sector matures, the gap between the best-practice operators and average performers will likely widen. Insurance markets will continue developing more sophisticated tools to identify and reward operational excellence, creating competitive advantages for asset owners who demonstrate true resilient behavior.

That’s not fear-mongering, that’s the reality of hail. As climate change continues to change our weather patterns, we find that 100% of solar sites across the country will see some damage-level hail near the site in the next 25 years.

kWh Analytics’ CEO, Jason Kaminsky, breaks down these risks and others reported in the 2025 Solar Risk Assessment with SunCast host Nico Johnson.

The 2025 Solar Risk Assessment report, recently released by kWh Analytics, has sparked significant discussion among industry professionals about the evolving challenges facing renewable energy assets. To explore the report’s findings in depth, kWh Analytics convened its Renewable Energy Broker Council, bringing together leading insurance brokers specializing in solar and battery storage to share their perspectives on the industry’s most pressing risks. The council provided a platform for these experts to discuss the implications of the report’s findings and identify strategies for stakeholders.

The Broker Council consisted of the following participants: Rob Battenfield (AmWins), Todd Burack (McGriff), Mike Cosgrave (Renewable Guard), Brian Fitzgerald (WTW), John Katilus (Aon), Geraldine Kerrigan (CAC Specialty), Alex Post (Alliant), and Luke Slemeck (Marsh).

Advancing Hail Risk Mitigation

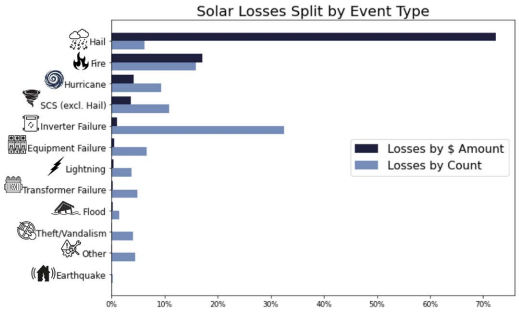

The 2025 Solar Risk Assessment highlighted hail as the dominant cause of solar losses, accounting for 73% of total losses by damage amount despite representing only 6% of loss incidents. This finding resonated strongly with the brokers, who emphasized the critical importance of robust hail defense strategies and the evolution toward more data-driven approaches.

Distributions of loss counts and losses by $ amount incurred, by different event types. Source: kWh Analytics 2025 Solar Risk Assessment

Mike Cosgrave from Renewable Guard emphasized how clients are embracing more sophisticated risk engineering: “What’s really resonating with our clients is asking resources, like VDE Americas, to rerun models to see the effects of resilience measures like thicker modules and different stow angles on Probable Maximum Losses (PMLs, an important metric in insurance). In some cases, our clients are collaborating with us very early in the process. Design and equipment decisions are being made on this basis very early in the development process. For the Sponsors, it’s both a question of cost benefit, along with an overall desire to reduce risk. That’s where I’m seeing a lot more collaboration between insureds and others in the industry.”

The council discussed how the industry has moved towards implementing comprehensive hail defense protocols that demonstrate measurable risk reduction.

Technology Selection and Market Access

Much of the discussion centered on how module selection and technology choices are increasingly becoming essential to obtaining reasonable insurance coverage. The conversation revealed a shift in market dynamics, as Todd Burack from McGriff highlighted: “As insurers have become more sophisticated, site resiliency becomes less of an option, because without it, insurance just won’t participate. There is a price of admission to have a resilient asset, and it’s effectively building competition in the marketplace.”

This shift represents a maturation of the insurance market, where carriers are moving beyond simply pricing to the standard, to differentiating premiums based on specific resilience measures, such as thicker glass modules in hail-prone regions. Projects with legacy technology or inadequate resilience measures may find themselves unable to secure coverage at any price, fundamentally changing how developers approach equipment selection and project design.

The Insurance Procurement Challenge

Despite significant investments in resilience technology and engineering analysis, brokers identified a disconnect between technical risk assessments and insurance purchasing requirements. This gap has created frustration among developers who invest in sophisticated risk mitigation measures but don’t see corresponding reductions in coverage requirements.

Luke Slemeck from Marsh highlighted this industry challenge: “Today, asset owners invest in hail resilience with racking systems that stow at 50 degrees or greater, and have independent engineers run PML loss studies to show their benefits, yet insurance limits are sized well above the stowed PMLs. Somewhere along the line, independent insurance advisors are ignoring the realities of what developers on the ground are being asked to do: to design for resilience, causing insureds to buy much greater limits than the PML studies indicate are appropriate.”

The brokers acknowledged that navigating these conflicting requirements puts them in a challenging position between their clients’ interests and conservative industry standards. Brian Fitzgerald from WTW emphasized the broker’s responsibility in these situations: “We have that fiduciary responsibility to help clients buy the right amount of insurance, not to inflate coverage unnecessarily. When interested parties require certain coverage levels, it can be hard to push back, but it’s incumbent on experienced brokers to advocate for their clients when the data supports it, even though it can be a contentious process.”

This disconnect highlights the need for better alignment between engineering assessments, insurance requirements, and actual risk profiles of modern resilient solar projects.

Battery Energy Storage Systems: Navigating Early-Stage Risks

The rapid growth of battery energy storage systems featured prominently in the discussion, with brokers sharing firsthand experiences about the critical importance of the commissioning and early operational phases. EPRI’s findings in the 2025 Solar Risk Assessment, noting that 72% of BESS failures occur within the first two years, resonated strongly with the group.

John Katilus of Aon offered insights from direct loss experience: “Aon’s claims team has seen a small number of hot commissioning losses of Battery Energy Storage System (BESS) farms.”

“Hot testing” generally refers to the phase where the BESS system is energized and begins operating with the intended power sources and control systems. It’s the critical step where the entire system, including the Battery Management System (BMS), Power Conversion System (PCS), and plant controllers, is tested under real-world conditions.

Faulty workmanship appears to be one of the leading contributing loss factors. The hot commissioning period is also one of the riskier phases during a construction project cycle. A phased approach during commissioning, as opposed to commissioning the entire site, will significantly limit the overall loss expectancy exposure.

Data Quality and Risk Assessment Challenges

The brokers strongly supported the insurance industry’s move toward more sophisticated risk assessment, highlighting ongoing data collection and standardization challenges.

Rob Battenfield of AmWins highlighted the disparity in market approaches: “Not all insurance stakeholders understand how to ask the right questions and put data together in a way to differentiate clients in the eyes of an underwriter. Committed brokers in the space sit in a unique position where they have the ability to really make a difference. Experts can not only assist in designing efficient risk transfer but also communicate best practices in risk mitigation.”

The discussion also revealed challenges around having extensive data without clear decision-making frameworks. Alex Post noted the data paradox that the industry is facing: “We have almost too much data and often conflicting modeling information, creating uncertainty about what data should be trusted and making it difficult for asset owners to make informed insurance decisions. The risk exposure level changes significantly based on equipment and resilience tactics deployed on site. With solar, the challenge is finding a fair balance between managing these shifting exposures (based on stow angles, risk mitigation, etc.) and the financial security that stakeholders seek under adverse loss scenarios.”

The brokers also made a call to action for the industry to improve data collection and documentation. Geraldine Kerrigan from CAC Specialty highlighted a key missing element: “We would love to see clients provide us information on when hail falls and nothing happens—that’s actually more interesting than when it falls and something does happen, but we don’t get that data.”

These positive case studies of successful risk mitigation could help demonstrate the value of resilience investments and push the industry toward more nuanced risk assessment approaches.

Future Outlook and Industry Recommendations

Here are the key takeaways from the discussion:

For Developers and Asset Owners: Invest in resilience measures early in the development process and maintain comprehensive documentation of risk mitigation efforts. Focus on proven technologies and robust operational protocols, particularly for projects in previously undeveloped areas.

For the Industry: Develop standardized approaches to measuring and valuing resilience, particularly for emerging technologies like BESS. Improve data sharing on both successful risk mitigation and loss events to create industry-wide learning opportunities.

For Insurers and Brokers: Continue advancing premium differentiation that properly rewards proactive risk management while working to simplify decision-making frameworks that can handle increasingly complex technical data.

The renewable energy sector’s continued growth depends on building infrastructure designed to withstand evolving climate and operational challenges. While significant progress has been made in understanding and managing risks, the industry must continue adapting as we face changing natural catastrophe profiles.

Here’s the clear path forward for the industry: continue to collaborate, focus on data-driven decision making, and prioritize proactive risk management.

2025 Solar Risk Assessment Report highlights challenges and opportunities to the renewable energy sector as solar and battery storage play a more prominent role in supporting the electrical grid.

Industry collaboration remains key to building resilient assets.

June 10, 2025

SAN FRANCISCO – kWh Analytics, the leading provider of Climate Insurance and risk management solutions for renewable energy, today released its 7th annual Solar Risk Assessment (SRA), a comprehensive report designed to provide an objective, data-driven evaluation of solar and battery energy storage systems (BESS) risk. The annual report includes contributions from academia, technology, financing, and insurance leaders in the solar energy and BESS industries.

“As renewable energy becomes the backbone of the electrical grid, ensuring system resilience is no longer optional—it’s imperative,” said Jason Kaminsky, CEO at kWh Analytics. “Keeping these assets operational requires unprecedented collaboration among asset owners, operators, financiers, insurers, brokers, and manufacturers. We are grateful for the valuable research and articles by this year’s Solar Risk Assessment contributors, who are helping to establish higher industry standards required to build infrastructure that withstands heightened risks.”

The 2025 report consists of 15 articles written by U.S. and global industry partners and provides an objective analysis of the top extreme weather, operational, and battery risks facing the renewable energy sector. Top findings by category include:

Extreme Weather Risk

kWh Analytics: Hail accounts for 73% of total losses by damage amount, despite representing only 6% of loss incidents

Central Michigan University: 99.27% of PV plants have a 10% annual chance of seeing Hail bigger than 2 inches in their close proximity

Kiwa PI Berlin: Cross-cutting analysis reveals frame to glass deviations exceed 5% of acceptable thresholds, highlighting needs for additional quality control & module testing

60Hertz Energy: Projects can experience 6% revenue annual loss from far away wildfire smoke

VDE Americas: Study Shows 100% hail stow success despite severe storm exposure

kWh Analytics and GroundWork Renewables: The risk of inelastic behavior: Physics-based models may be overestimating the benefit of hail stow by 48% for ~3in hail

Operational Risk

kWh Analytics: PV sites around the country are underperforming by 8.6% on average

Zeitview: Hot spot prevalence on sites increased from 0.24% in 2023 to 0.81% in 2024: A Sample of Newly Commissioned Sites in North America

Clean Power Research: Future climate models suggest potential -4.9% impact to PV production

kWh Analytics: AI models misclassify up to 20% of solar operational issues without domain-specific training

Battery Risk

Clean Energy Associates: 28% of energy storage systems show fire suppression issues during 2024 factory inspections

EPRI: To date, 72% of BESS failures have occurred within the first 2 years of installation

Accure Battery Intelligence: State of Charge (SOC) estimation errors for LFP batteries can exceed 15%

TWAICE: Lost in translation? O&M teams see up to 2x more BESS issues than asset managers

“Insurance plays a key role in protecting our infrastructure,” said Isaac McLean, Chief Underwriting Officer, kWh Analytics. “The Solar Risk Assessment enables us to identify emerging risks and understand what data we need to inform accurate underwriting and promote resiliency among project developers and asset owners.”

Key takeaways from the 2025 report include:

Hail continues to represent one of the most severe financial risks. Implementing proper module selection with thicker glass and advanced stow protocols that allow for steeper tilt angles can significantly reduce damage probability during severe storms.

While the emergence of AI technologies presents powerful opportunities for renewables, improperly trained models can give false results. Data quality will be imperative to incorporating these tools into the industry.

Cyber threat activity targeting renewable energy infrastructure is growing, necessitating enhanced protection strategies.

Quality inspections of energy storage systems identify issues with fire suppression systems and thermal management components, highlighting the critical need for improved manufacturing and monitoring systems.

kWh Analytics, a leading Climate Insurance provider, underwrites property insurance and revenue firming products for renewable energy assets. Our proprietary database of 300,000+ zero-carbon projects and $100B in loss data fuels advanced modeling and insights, enabling precise underwriting decisions. This data-driven approach incorporates resiliency measures in risk evaluation, promoting sustainable practices in the renewable energy sector.

Trusted by 5 of the top 10 global (re)insurance carriers, we’ve insured over $50 billion in assets to date. Our tailored solutions further our mission of providing best-in-class Insurance for our Climate. Recognized by InsuranceERM Climate and Sustainability Awards, kWh Analytics continues to pioneer in the renewable energy insurance sector.